Industry at a glance

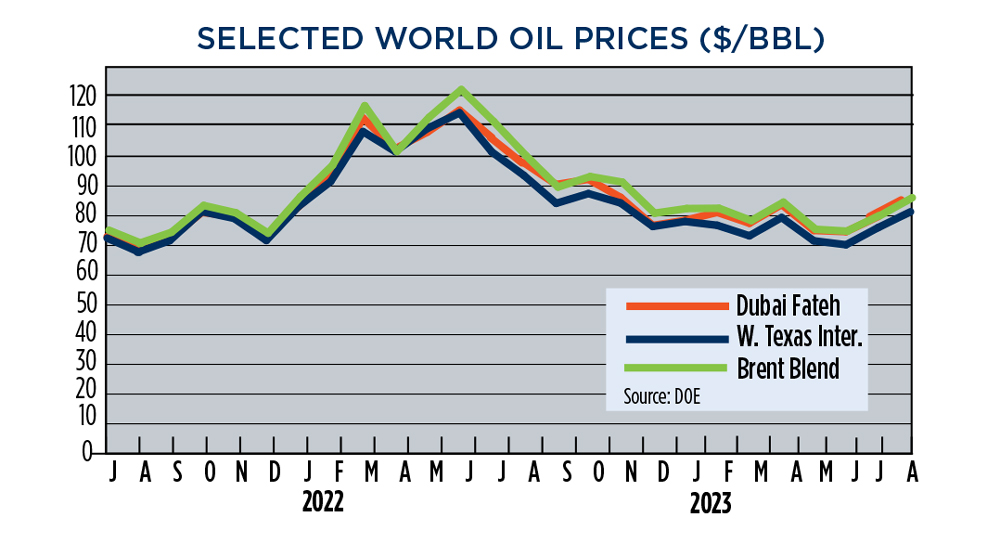

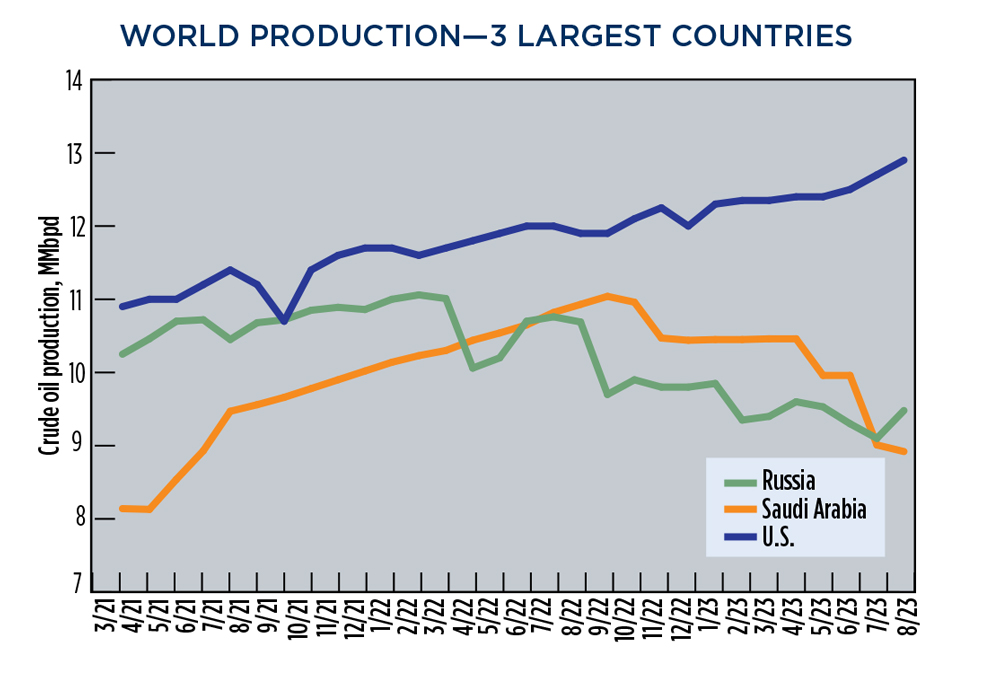

OPEC+ continued to reduce oil supply during a period of record demand, which was sparked by an increase in Chinese consumption and an uptick in petrochemical feedstock requirements. Global crude markets are forecast to have a supply shortfall of 1.2 MMbopd by yearend as Saudi Arabia extended its production cuts causing concern about commodity availability. The downward pressure on inventory caused benchmark crude prices to surge in August, with Brent up 7.5% to $86.15/bbl with WTI jumping 7% to average $81.39/bbl. This is the second consecutive month both global benchmarks experience a significant price increase (Brent +7%; WTI +8% in July). Prices are expected to rise further as Brent futures hit a 10-month high of $92/bbl for fourth quarter delivery.

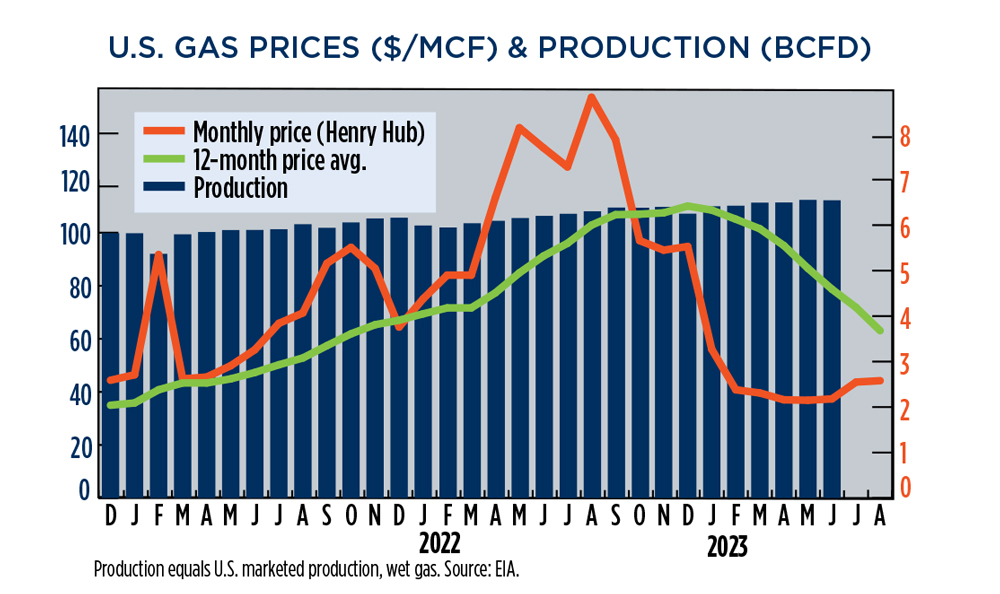

U.S. natural gas outlook. U.S. natural gas prices remained depressed in August despite prolonged record heat in a large portion of North America over the last several months. The market showed no signs of recovery with the commodity at Henry Hub trading at $2.58/MMBtu in August, compared to $2.55/MMbtu in July. Despite short-term price stability, the 12-month running average at HH plummeted 12% in August, down to $3.68/MMBtu documenting the protracted price decline since August 2022 when operators were receiving $8.81/MMBtu for product.

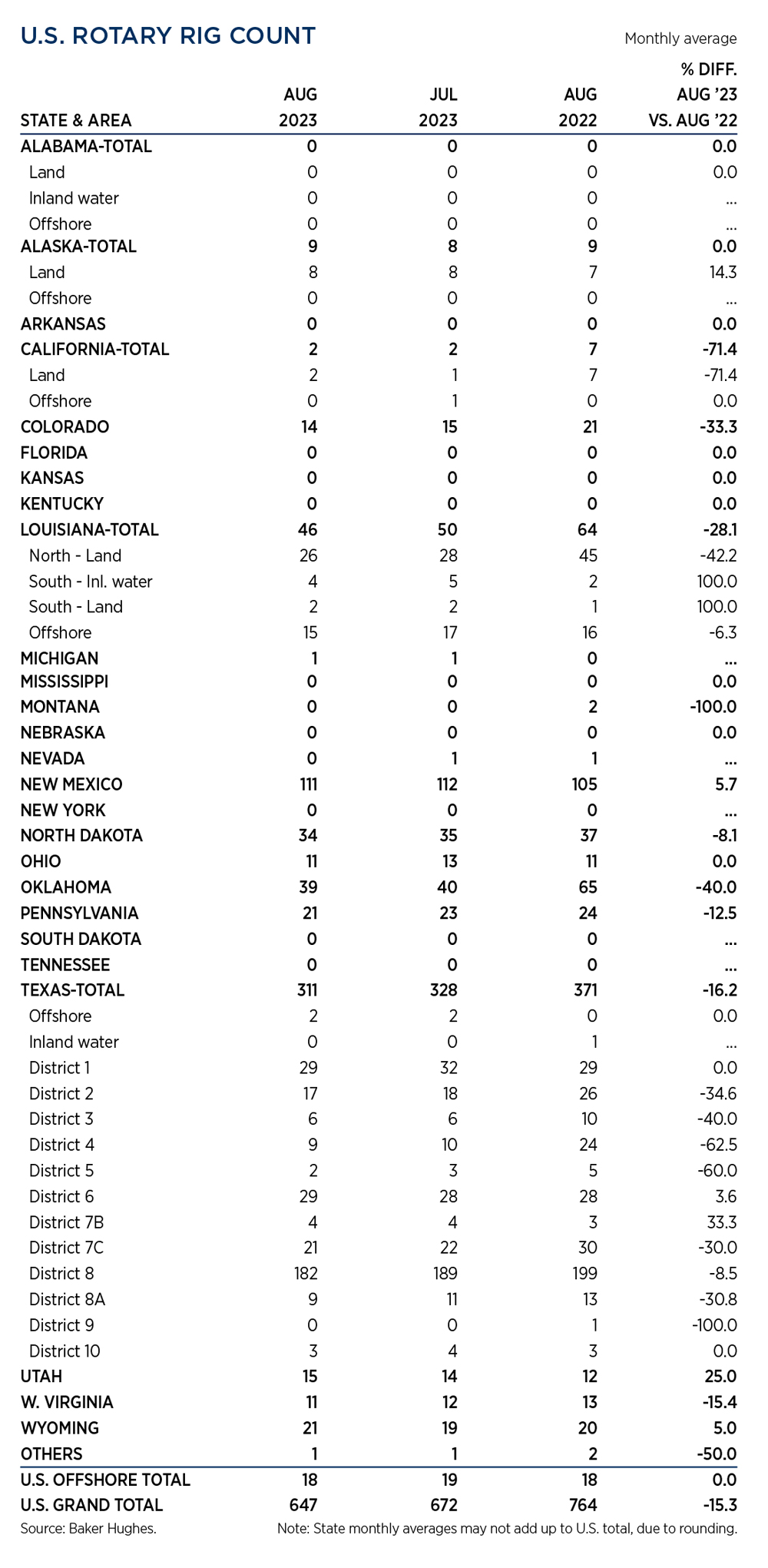

U.S. rig count. The back-to-back increase in crude prices did nothing to lift U.S. drilling activity, with the rig count dropping 25 units in August, down to 647 after losing 15 rigs in July (672). The overall Texas count declined 17 rigs to 311, with a seven-rig loss reported in RRC District 8, dropping to 311. A three-rig decline occurred in District 1 (29) with District 8A losing two rigs down to nine. Activity in Louisiana also slumped, with the Pelican State suffering a four-rig decline down to 46. In Northern Louisiana’s Hansville district, activity has plummeted 42% on a y-o-y basis with depressed gas prices forcing operators to stack an average of 19 rigs over the 12-month period.

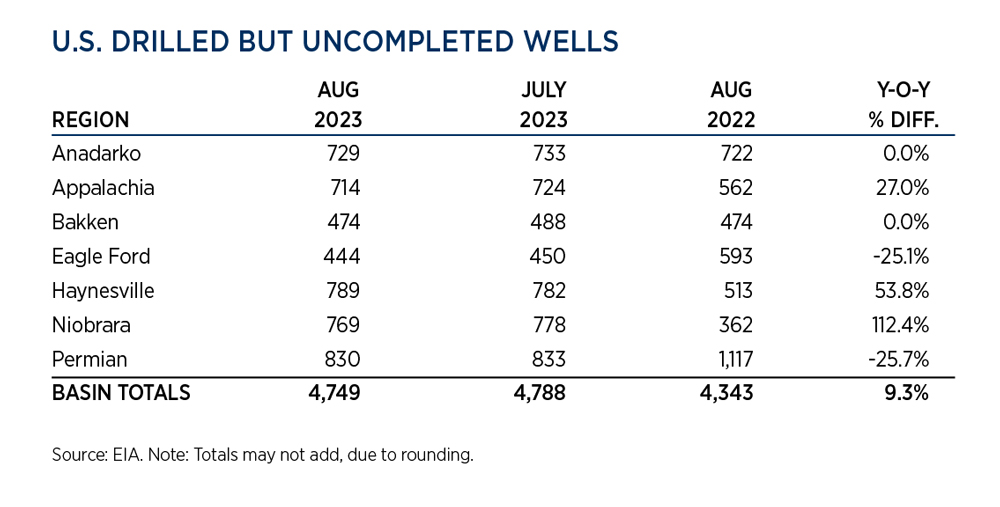

Drilled but uncompleted. Despite depressed U.S. natural gas prices, operators continue to drill in gas dominated regions, but with less intensity. DUCs in the major oil plays continue to drop, but not as rapidly as in previous months. In August 2023, there were 4,749 DUCs in the U.S., 406 more than the 4,343 tallied in August 2022 (+9%). In recent months, the build in the DUC inventory has moderated, but only two of the seven regions mapped by EIA show y-o-y declines. In the Niobrara region, DUCs are up to 769 (+112%), the Haynesville region has 789 (+54%), Appalachia has 714 (+27%), with 474 DUCs reported in the Bakken inventory, the same as one year ago. On a positive note, the Permian and Eagle Ford experienced y-o-y declines of -26% and -25% in their DUC inventories, respectively.

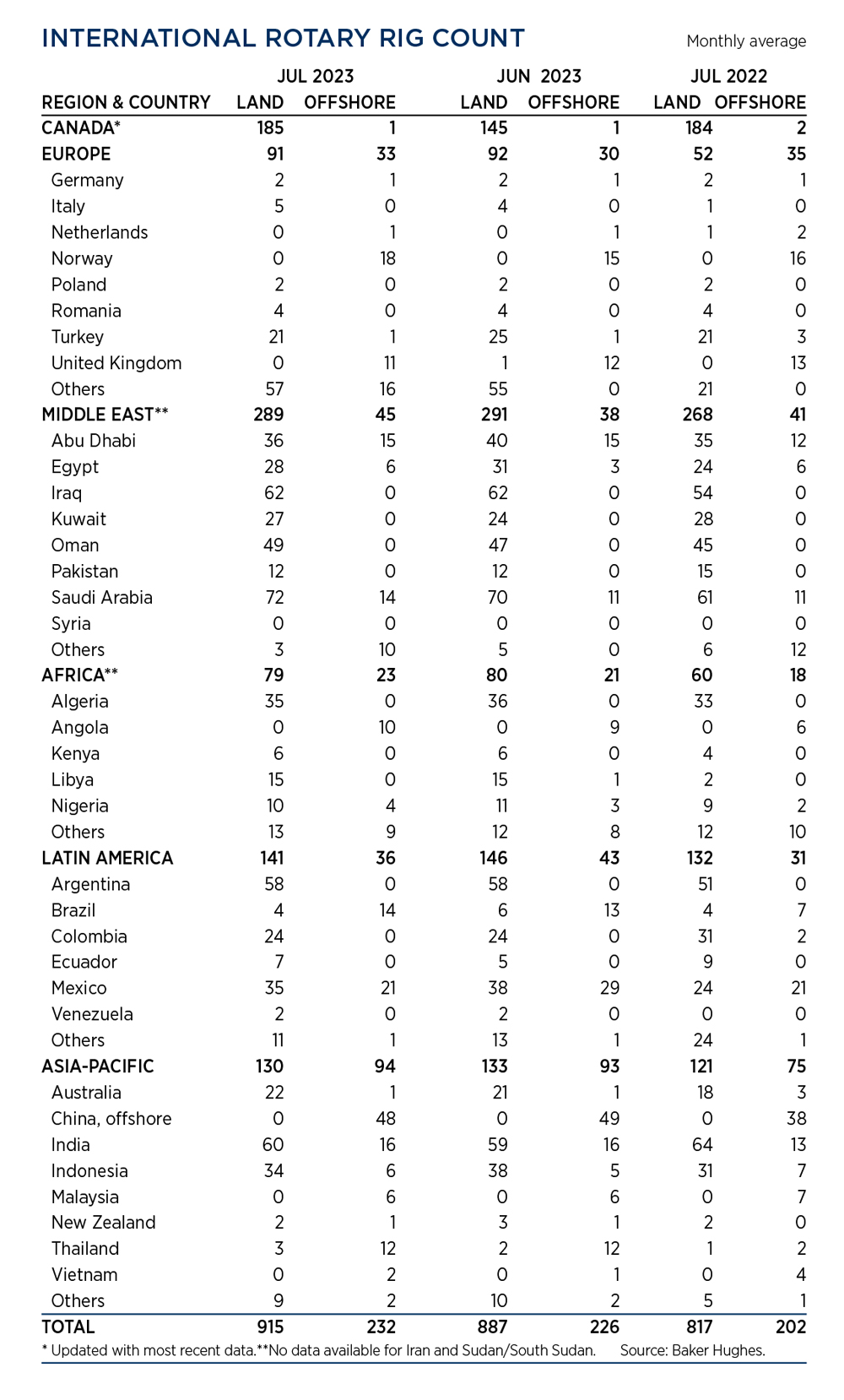

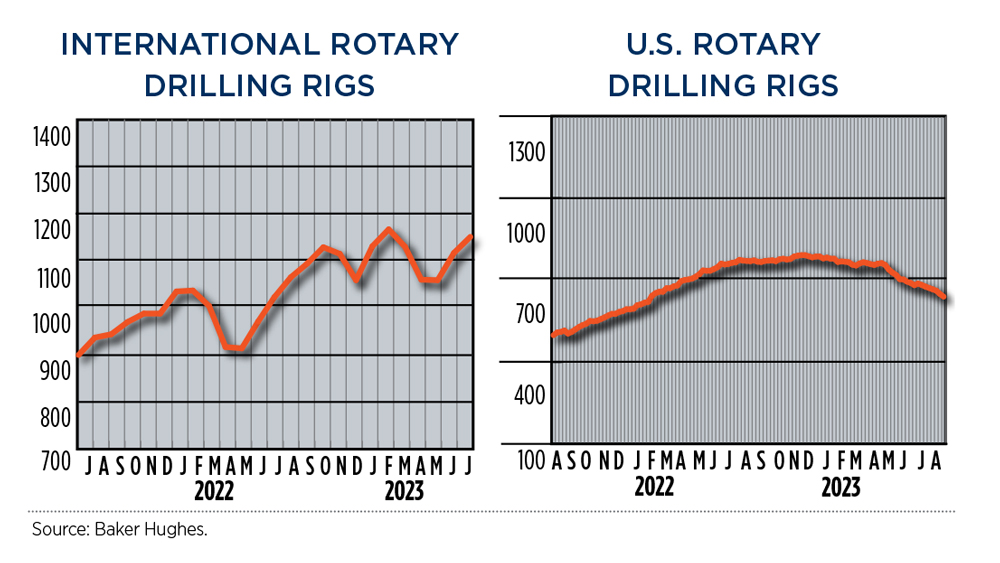

International rig count. Similar to last month, drilling activity outside the U.S. remained relatively steady with the exception of Canada. In July, the international rig count averaged 1,147, 34 more than the 1,113 working in June. The largest gain was once again reported in Canada, where operators put 40-rigs back to work as summer heat continued to harden muddy lease roads.

The increase in Canada was offset by a decline in Latin American activity, which was down five land-based rigs to average 141 in July. Mexico accounted for the majority of the loss, dropping three-rigs to 35. In the Middle East, land-based activity declined by four rigs in Abu Dhabi (36), while Egypt suffered a three-rigs loss to average 28 in July.

- Dallas Fed: Outlook improves, even as activity little changed; break-even prices increase (April 2024)

- The last barrel (February 2024)

- Oil and gas in the Capitals (February 2024)

- What's new in production (February 2024)

- First oil (February 2024)

- E&P outside the U.S. maintains a disciplined pace (February 2024)

- Applying ultra-deep LWD resistivity technology successfully in a SAGD operation (May 2019)

- Adoption of wireless intelligent completions advances (May 2019)

- Majors double down as takeaway crunch eases (April 2019)

- What’s new in well logging and formation evaluation (April 2019)

- Qualification of a 20,000-psi subsea BOP: A collaborative approach (February 2019)

- ConocoPhillips’ Greg Leveille sees rapid trajectory of technical advancement continuing (February 2019)