Regional Report: Gulf of Mexico

As it turned out, 2016 was not the end of the world for Gulf of Mexico (GOM) E&P. Even more encouraging, there’s talk of recovery just around the corner. But there’s still plenty of caution in that outlook.

OPTIMISM IS A POSSIBILITY

Deep layoffs and cost-cutting, which dominated the industry this time last year, may be giving way to the underlying long-term resiliency of deepwater operations. Despite the downturn, big projects continue to churn ahead. Nevertheless, the impact of market turmoil on project economics, emphasis and timetables is likely to moderate any recovery for many years to come. In aggregate, the universe of opinions and predictions appears to support either a mood of cautious optimism or moderated pessimism.

Last year, GOM activity dropped to a low of 117 wells. This year, World Oil projects a 9% increase to 128 wells. Most of that is coming from deepwater development activity already underway. While anemic, rig activity appears to have steadied. The Baker Hughes rig count on Feb. 17, 2017, had 17 rotaries working in the GOM, eight less than in 2016; which was down a whopping 27 rigs from 2015. (The highest on record is 128 rigs in January 2001; the lowest is nine in August 1992.)

IHS Markit’s Petrodata rig tally for Feb. 17 counted 98 units and a utilization rate of 71.7%, in contrast to 123 units in 2016 year and a utilization rate of 66.7%. In 2015, the utilization rate was 79%. Globally, the Feb. 17 Petrodata utilization rate was 68.9%.

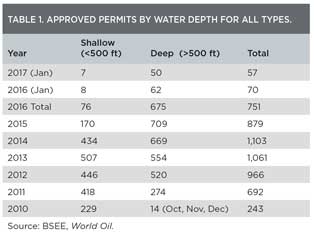

Drilling permits issued by the Bureau of Safety and Environmental Enforcement (BSEE) tailed off in 2016. Deepwater permits fell from 709 in 2015 to 675 in 2016, and shallow permits continued to decline from 434 in 2014, to 170 in 2015, and just 76 in 2016. The January 2017 total was 13 less than January 2016, Table 1.

A lease sale this year may provide some insights on industry enthusiasm. Sale 249 is tentatively scheduled for August 2017, pending the environmental impact statement and choosing one of five alternative plans. The last lease sale, 248, in August 2016, garnered $18,067,020 in high bids for 24 tracts covering 138,240 acres in the Western Gulf area.

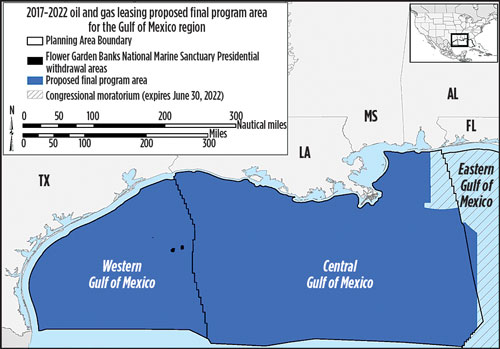

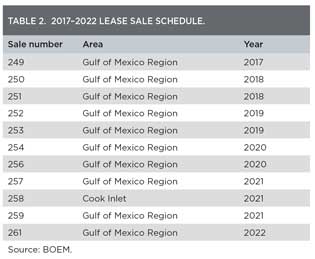

The Bureau of Ocean Energy Management’s (BOEM) new 2017–2022 GOM leasing program includes 10 proposed sales—one, each, in 2017 and 2022, and two sales, each, in 2018, 2019, 2020 and 2021, Table 2. The sales are all in the Central and Western program areas, Fig 1.

A WORD OF CAUTION

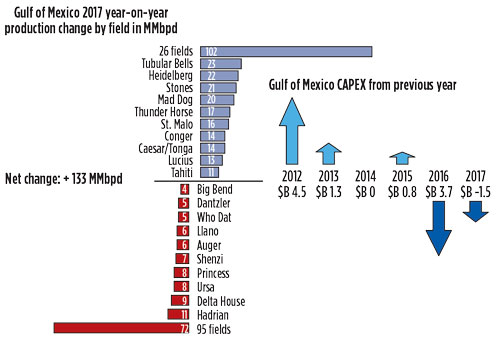

The belt-tightening will continue in 2017, as investment dollars are reduced and project priorities change, according to analysts at Wood Mackenzie. The firm predicts lower oil prices, and the end of a major investment cycle in the deepwater GOM “will finally take its toll on the region.” They expect 2017 investment to drop to $10 billion, a 36% decline from the 2015 peak and the lowest since 2011, Fig. 2.

The overall average rate for rigs in the GOM is much higher than current day rates because of existing contracts, said the company. As a result, a $200,000-difference will result in contract cancellations and renegotiations in 2017. While lower rig rates will reduce well costs, Wood Mackenzie believes operators also will have to reduce project design costs. “Reducing well count by high-grading development well locations, and completing exploration and appraisal wells, will further help as companies prioritize lowering break-evens, instead of increasing ultimate recovery.” In this environment, said analysts, exploration will remain a low priority, and independents are expected to focus limited budgets on development activities.

POSITIVE SIGNS

On the other hand, increased global capex spending and higher oil prices are positive factors for the GOM E&P outlook. In World Oil’s February issue, in the forecast of 2017 capital spending, Evercore ISI analyst James West said he expected a global increase of 1.7% this year. That follows decreases in upstream spending of 27% in 2016 and 21% in 2015. A positive note is also found in the recent OPEC production deal that caused an 8%-plus recovery in crude prices. West noted that the working rig count in the GOM appeared to have leveled out in the third quarter of 2016, and that rig supply had stabilized, with newbuilds balancing with cold-stacked rigs.

PRODUCTION GROWTH

U.S. crude oil production averaged 8.9 MMbpd in 2016, a decline of 500,000 bopd from 2015 levels, according to the U.S. Energy Information Administration (EIA). However, EIA said end-of-year data suggest that production began increasing in fourth-quarter 2016, averaging 8.9 MMbopd for the quarter, up from an average 8.7 MMbopd in the third quarter. Most of the fourth-quarter increase came from the federal GOM, although Lower 48 onshore production may have added almost 60,000 bopd.

GOM production is forecast to average 1.63 MMbopd in 2017, up 100,000 bopd from 2016, but 100,000 bopd lower than EIA previously expected. In 2018, production is expected to grow to 1.77 MMbopd, down 90,000 bopd from the EIA’s previous forecast. The net result is an expectation that total U.S. crude oil production will average 8.98 MMbpd in 2017 and 9.53 MMbpd in 2018, levels that are 20,000 bpd lower and 230,000 bpd higher, respectively, than previously forecast.

EIA said the anticipated expansion of Tahiti field is expected to contribute to the increase in the Gulf’s production, as are the start of production from Horn Mountain Deep field in 2017 and the Big Foot and Stampede projects in 2018, along with other projects that will begin operations in 2017 and 2018.

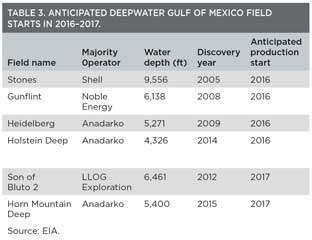

Start-ups in 2017 include LLOG Exploration’s Son of Bluto and Horn Mountain Deep fields, the latter now Anadarko’s project after acquisition of Freeport McMoRan’s deepwater GOM properties, Table 3. The EIA forecast cited 14 deepwater projects: nine in 2015; four in 2016; and one in 2018.

Chevron’s Big Foot development was delayed by damage to the TLP’s subsea installation tendons. It is now expected to come on stream in 2018. The facility is in Walker Ridge Block 29, in approximately 5,200 ft of water and will produce from 16,000 ft.

Hess’s Stampede project, where first oil is also expected in 2018, plans to install a TLP and topsides on location, and complete subsea installation, in 2017. Earlier this year, production services firm Danos announced that it had secured the contract to perform mechanical hook-up and commissioning support services for the TLP.

ACTIVE OPERATORS

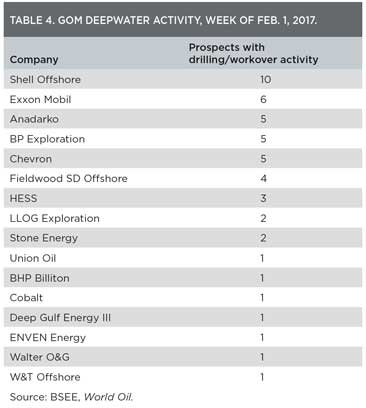

The first week in February 2017, BSEE counted 49 deepwater prospects with drilling and workover activity, Table 4. The top five active companies were Shell Offshore, Exxon Mobil, Anadarko, BP Exploration and Chevron, with prospects including Stones, Mars, Perdido, Julia, Shenandoah, Fourier and Sawtooth.

DEEPWATER PROJECTS OVERVIEW

Shell expects its Stones field to be producing 50,000 boed when it is fully ramped up at the end of 2017. Production began Sept. 6, 2016. Stones is the world’s deepest-water oil and gas project, operating in approximately 9,500 ft of ocean.

All eight Lower Tertiary wells that Shell plans for Stones field will be connected to the FPSO Turritella. Named for a genus of Tertiary age snail, the Turritella is Shell’s 13th FPSO. The vessel arrived in the Gulf in January 2016.

In early June, InterMoor completed the final tensioning and chain-cutting operations. The Turritella is a disconnectable turret-moored FPSO. It has nine mooring lines consisting of chain and polyester, arrayed in three bundles of three. The mooring lines were attached to a disconnectable Buoyant Turret Mooring (BTM) buoy in the field, awaiting the FPSO’s arrival.

The turret allows the vessel to weathervane in normal conditions and disconnect entirely in hurricane conditions. Stones’ riser is a lazy wave riser configuration, with a steel catenary riser with buoyancy added, and an arch bend to decouple the FPSO’s dynamic motions and improve riser performance. The Stones project is 100% owned and operated by Shell, and is the company’s second producing field from the Lower Tertiary, following the start-up of Perdido in 2010.

Shell’s Appomattox deepwater development, announced in 2015, is under construction, with production targeted for 2020. It is the company’s eighth and largest floating platform in the Gulf, with a capacity of 175,000 boed.

In July 2016, Shell reported a new deepwater GOM discovery, with initial, estimated recoverable resources of more than 125 MMboe. The Fort Sumter well was drilled in Mississippi Canyon Block 566 in water depth of 7,062 ft, to 28,016 ft, MD. Further appraisal drilling is planned in adjacent structures.

Noble Energy’s Gunflint oil development began producing in July 2016. The ramp-up of the two-well field is expected to reach a minimum gross production of 20,000 boed. The development, in Mississippi Canyon Block 948, is a subsea tie-back to the Gulfstar One facility owned by Williams Partners L.P. and Marubeni Corporation.

“The Gunflint project marks our fourth successful offshore major project completed within the past nine months, including the start-up of Big Bend and Dantzler in the Gulf of Mexico as well as the non-operated Alba B3 compression platform in Equatorial Guinea,” said Hodge Walker, Noble Energy’s V.P. for the Gulf of Mexico and West Africa. Gunflint is a subsalt Miocene discovery in Mississippi Canyon Block 948. It was drilled in 2008 to approximately 29,280 ft, TD, where more than 550 ft of net hydrocarbons were found in multiple reservoirs. Two appraisal wells were drilled and evaluated in 2012 and 2013.

The pipeline ties back to Williams Partners’ Gulfstar floating production system (FPS), which has a base design for up to 60,000 bopd and 135 MMcfgd. The floating spar was moored on-site in February 2014, in about 4,300 ft of water. The hub handles production from Hess and Chevron’s Tubular Bells field to feed Williams’ downstream gathering and processing facilities.

Anadarko doubled its ownership in the Lucius development to 49% and added approximately 80,000 net boed in a $2.0-billion deal that acquired Freeport-McMoRan Oil & Gas’s deepwater GOM properties. The transaction was effective as of August 2016 and closed in December. At the end of the 2015, Freeport-McMoRan said its deepwater GOM areas included Lucius in Keathly Canyon; Holstein, Holstein Deep, and Heidelberg in Green Canyon; and Vito, Horn Mountain, King, and KO/QV in Mississippi Canyon.

Anadarko Chairman, President and CEO Al Walker, called the Freeport-McMoRan deal an “immediately accretive, bolt-on transaction.” The transaction expands Anadarko’s infrastructure in the Gulf, adding to subsea tie-back opportunities and improving new exploration options. With the addition of these properties, Anadarko said it has net sales volumes of approximately 155,000 boed, comprised of approximately 85% oil.

Based on Lucius reservoir performance and facility productivity, Anadarko increased the estimated ultimate recovery to more than 400 MMboe from the previous 300-plus MMboe. Gross oil sales volumes through the facility surpassed 100,000 bopd in third-quarter 2016. The company said the field’s cash flow would be directed to the onshore Delaware and DJ basins.

Anadarko reported first oil from the Lucius spar’s sister development, Heidelberg, in January 2016. It started production in January 2015. The spars have design capacities of 80,000 bopd and 80 MMcfgd. In late 2016, the field’s fifth production well encountered more than 150 net ft of oil pay on its way to a planned completion in early 2017.

Anadarko announced in December 2016 that its Warrior exploration well had encountered more than 210 net ft of oil pay in multiple high-quality Miocene-aged reservoirs. The discovery is a few miles from the Anadarko-operated K2 field, and is expected to be tied back to the Marco Polo production facility. Anadarko is the operator at Warrior with a 65% working interest. Other partners include Ecopetrol (20%) and Mitsubishi Corporation Exploration Co., Ltd. (15%). Anadarko previously announced that its Phobos appraisal well, 12 mi south of the Lucius facility, encountered more than 90 net ft of high-quality oil pay, while drilling to a Wilcox objective.

The LLOG-operated Delta House floating production system (FPS) at Mississippi Canyon 254 achieved its nameplate oil capacity of 80,000 bopd in January 2016. First production occurred in April 2015. The FPS draws from three fields: Son of Bluto, Marmalard, and Otis. Addition of production from two more wells was expected. The FPS is designed for peak capacity of 100,000 bopd and 240 MMcfgd. ![]()

Mexico awards deepwater properties

Mexico awarded eight of 10 deepwater exploratory blocks in December 2016, with estimated reserves of 11 Bbbl. Two of the blocks received no bids.

“This is a vote of confidence that the energy reform is moving forward and for the geological potential of the Mexican Gulf deep waters… everybody paid a premium and that premium indicates the potential of the blocks,” said Jorge R. Piñon, former president of Amoco Oil Latin America and now an analyst at the University of Texas at Austin, in a New York Times article.

All four blocks in the Perdido basin, which spans the maritime border, were leased to companies including Total, CNOOC, Chevron and Exxon Mobil. Drilling on the U.S. side of the line has been successful. Four of six blocks were awarded in the less-explored Salina basin to companies including Total, Statoil and BP. BHP won rights in Trion field, along with Pemex.

In late December, Mexico said it would delay announcement of its Round Two tender winners to improve participation. Originally planned for March, the delay will move to June, the announcement of winners of 15 shallow-water areas in the Tampico-Misantla, Veracruz and Cuencas del Sureste regions.

The deepwater auction is the fourth public tender. Three prior auctions have involved shallow-water and onshore blocks. In 2014, Mexico approved opening the country’s oil and gas industry to foreign investment for the first time since 1938. The first public tender in July 2015 offered 14 shallow-water blocks and awarded only two on the GOM’s southern rim. However, the deepwater fields will probably not produce significant oil for at least a decade.

The auctions were the result of Mexico instituting energy reform legislation in 2013 and 2014, which ended the 75-year-old monopoly of Pemex and opened the country to foreign investment for oil and gas ventures. The effort was viewed as the only way to end years of declining production. ![]()

- Applying ultra-deep LWD resistivity technology successfully in a SAGD operation (May 2019)

- Adoption of wireless intelligent completions advances (May 2019)

- Majors double down as takeaway crunch eases (April 2019)

- What’s new in well logging and formation evaluation (April 2019)

- Qualification of a 20,000-psi subsea BOP: A collaborative approach (February 2019)

- ConocoPhillips’ Greg Leveille sees rapid trajectory of technical advancement continuing (February 2019)