Iran conflict: Global oil prices surge but not as much as feared, so far

UPDATE: The unprecedented military action launched by the U.S. and Israel against Iran on Saturday, Feb. 28, has certainly shaken the global oil market out of its low-price mediocrity, at least temporarily. But the increase in oil prices on trading markets during Monday, March 2, has been less robust than many analysts feared. As of late morning, Houston time, the WTI price was trading at $70.78/bbl, up $3.81. Brent crude was at $75.79/bbl, up $3.50.

In a remarkable effort of military superiority, intelligence gathering/monitoring, and perfect logistics and timing, the U.S. and Israel on Saturday literally took out a majority of top Iranian leadership with one series of missile strikes on a governmental compound in Tehran. Killed in the attack were Iranian Supreme Leader, Ayatollah Ali Khamenei, along with at least seven members of his senior leadership team. According to the Trump administration, when one figures in a wider swath of leadership, at least 49 Iranian officials were killed in the initial wave of attacks. U.S. and Israeli forces also launched hundreds of missile and bomb strikes that affected at least 14 Iranian cities.

Despite the initial success of damaging the Iranian regime significantly, much remains to be done in terms of accounting for additional governmental officials, as well as the Islamic Revolutionary Guard Corps (IRGC). The devotion of the IRGC to Khamenei’s regime cannot be underestimated, and it may take a while to neutralize that force. One commentator on Fox News referred to the IRGC, which numbers nearly 40,000, as being like “an army within an army.” And remnants of the old regime continue to hurl missiles in all directions.

Oil market implications. Needless to say, the short-term effects of military actions in the Middle East could keep oil prices higher for a while. There is a nearly 53-year history of this cause-and-effect relationship, dating back to the Yom Kippur War of Oct. 6 to Oct. 25, 1973. Indeed, futures prices rose more than 2% on Friday, Feb. 27, in anticipation of eventual hostilities with Brent hitting $72.86/bbl (+2.45%), and WTI reaching $67.02 (+2.78%). But as noted, the price increases on Monday have failed to reach consensus expectations, much less the outlier predictions of $90/bbl (for Brent).

Of course, oil price behavior will depend on how long the military campaign might last, how much the flow of oil out of Iran is disrupted, and the war’s potential impact on the Iranian-controlled Strait of Hormuz. One thing is for certain—in the very short run, average gasoline prices across the U.S. are likely to go noticeably above $3.00/gal, compared to the current $2.98/gal level.

The OPEC+ angle. One factor that could help to slightly blunt a rise in oil prices is an action taken over the weekend by OPEC+ (OPEC, Fig. 1, and allied countries). A meeting on Sunday involved only eight members of OPEC+—Saudi Arabia, Russia, the UAE, Kazakhstan, Kuwait, Iraq, Algeria and Oman. OPEC and its allies said early Sunday they would raise its daily output by 206,000 bopd after pausing incremental production increases earlier in the year. In the fourth quarter, OPEC had boosted production by 137,000 bopd.

The production increase may have eased the surge in oil prices somewhat today, even though various energy analysts didn’t expect the production increases to do much to keep prices down. Ironically, Reuters reported that some of its sources had said that Saudi Arabia supposedly has been increasing oil production and exports in recent weeks by around 500,000 bpd, in preparation for U.S. and Israeli strikes on Iran. Given the additional spare capacity in the Kingdom, it is likely that Saudi Arabia and the UAE could put additional output on the market, if a supply shortage were to materialize for a significant period of time.

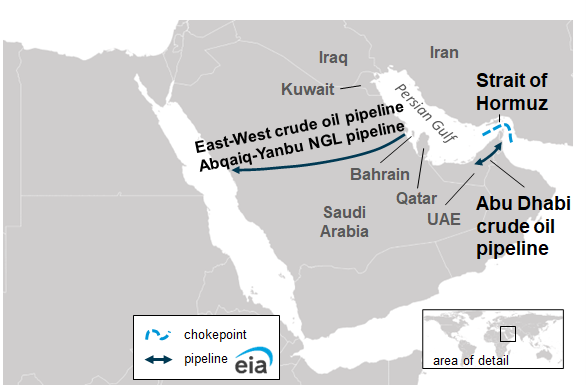

The Strait of Hormuz. This narrow waterway off Iran’s southern coast is the main shipping route for crude from oil-exporting countries Saudi Arabia and Kuwait to customers around the world. It can be said that Iran technically controls the strait’s northern side. According to the U.S. Energy Information Administration (EIA), roughly 20 MMbopd, or about one-fifth of daily global production, flow through the strait every day. For years, EIA has labeled the strait a “critical oil chokepoint,” Fig. 2. Indeed, the military actions of the last three days have pushed insurance premiums so high, that no tanker traffic is proceeding through the strait.

In previous disputes with the U.S. and other nations, Iran has threatened to close the strait. During the 12-day war with Israel and the U.S. last year, Goldman Sachs estimated that oil prices could go higher than $100/bbl, if the strait was closed or partially closed for an extended period. Meanwhile, Bob McNally, president of Rapidan Energy Group, told CNBC that he had advised clients for weeks that a military action in Iran was a 75% probability. He told the outlet that the current action is “a very serious development” for the global oil and gas markets, considering their dependence on

McNally and Andy Lipow, president of Lipow Oil Associates, said the attacks could significantly heighten the risk of an oil supply disruption in the region, even though Iranian oil facilities have not been directly targeted (so far). McNally and Lipow said the worst-case outcome would be an attack on Saudi oil infrastructure (in fact, an Iranian drone hit the Saudi oil refinery at Ras Tanura on Monday), followed by a complete closure of the Strait of Hormuz.” Lipow estimates the probability of that scenario at about 33%, given Iran’s current status. As McNally rightfully pointed out, facilities like the oil plant at Abqaiq field in Saudi Arabia, which was attacked in 2019, have custom-made equipment that cannot be ordered off the shelf from service-supply companies in the industry.

The China angle. It is a fact—China has been relying on Iranian oil for a while now. Indeed, Asian economies, including China and India, would be particularly affected, if the Strait of Hormuz were closed. China imported approximately 1.4 MMbpd of Iranian oil during 2025. It has been responsible for buying more than 80% of Iran’s ocean-borne crude exports. IN turn, Iranian oil represents more than 13% of China’s ocean-borne crude imports, and roughly one-third of China’s total oil imports go through the Strait of Hormuz.

Is it any wonder then, that China is scrambling to line up oil from other countries. And this could, in theory, send global oil prices higher. Even if only Iranian crude shipments are affected, it would have an effect on oil markets globally. In a recent research/opinion note written in anticipation of the U.S./Israeli attack, Clayton Seigle, a Senior Fellow and holder of the James R. Schlesinger Chair in Energy and Geopolitics at the Center for Strategic & International Studies (CSIS), noted, “…since oil is a global, fungible commodity, a disruption anywhere affects prices everywhere. A loss of Iranian barrels would cause China to bid for substitute supplies.”

Seigle worked up four potential scenarios for the current situation: 1) The U.S. or Israel disrupts Iranian crude oil shipments; 2) Iran disrupts Arab Gulf oil shipping; 3) The U.S. or Israel directly attacks Iranian oil facilities; and 4) Iran directly attacks Arab Gulf oil facilities.

Seigle says that scenario 1 is “reversible, meaning that the United States or Israel could call off its campaign against Iranian shipments at any time, with no permanent damage having been incurred and export volumes rebounding thereafter, like what was seen following the U.S. quarantine on Venezuelan oil shipments.”