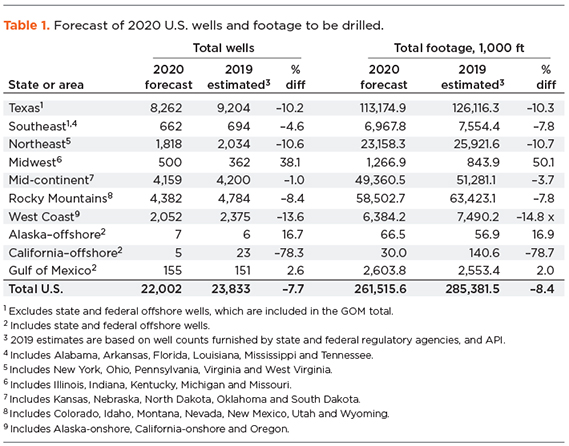

2020 Forecast - E&P spending

As 2019 came to a close, the global growth rate for oil and gas spending was set to come in at 3% versus 2018, a level that is moderately below global GDP growth and significantly less than our preliminary 8% forecast estimate a year ago. The main culprit driving this variance is North America (NAM), as global growth would have come in at 4.4% for 2019, if the U.S. and Canada had managed flat y-o-y results. Instead, NAM posted a year very different to the one prior, where we saw 20% y-o-y growth for 2018. We estimate that 2019 had a 6.5% reduction in spending, driven by a 6% decline in the U.S. and an 8.5% decrease in Canadian budgets. As we look at 2020, we foresee a similar story playing out in NAM. We project that Canadian budgets will improve marginally at 0.6%, y-o-y, for 2020, while the U.S. is set to decline 7.1%, leading to a 5.9% decrease for the broader region, Table 1.

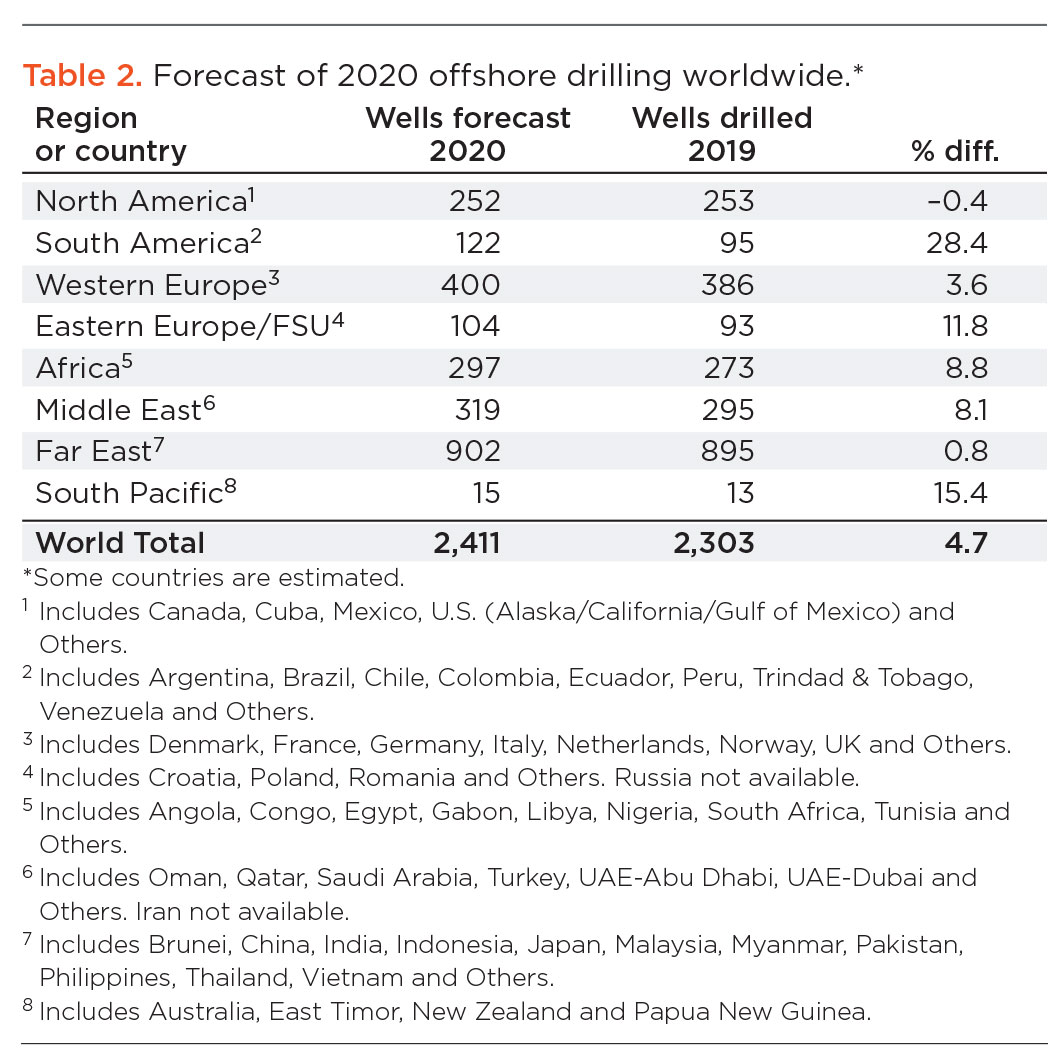

Investments go international. On the international scene, the story for upstream spending is much different. For 2019, we estimate that capex rose 6.3%, y-o-y, below our 7.2% y-o-y forecast last year. However, at this juncture, we moderate our forward outlook for international spending, as we go into 2020. But the story is still constructive, and we believe that unlike NAM, there are upside risks to our international forecasts for 2020. With higher spending needed just to maintain current production in U.S. shale, we believe that international and offshore will provide future output growth. For 2020, we forecast 4.9%, y-o-y, growth internationally, led by the Middle East and the super-majors, Table 2.

Loss of private equity funding. Bankruptcies among operators were trending higher during 2019, and the same is occurring for OFS companies. Among the two groups, a total of $20 billion in debt has gone through Chapter 11, and the figure goes to $175 billion, if the baseline is set in 2015. These numbers clearly indicate that capital has dried up, and private equity is not coming to the rescue.

Cash flow reigns supreme. With the industry’s focus on living within its means, it is not surprising that cash flow remained the number-one factor driving budgets for 2020. Over the past six years, cash flow has taken the crown, and its importance ramped up 23%, relative to last year’s survey. We believe this is a longer-term positive for the industry, as investors have told E&P management teams to learn to live within their cash flow, or else. Oil prices took the second-place spot for the second consecutive year, while capital availability rose in prominence, firmly securing its status in third place for the second year in a row.

Oilfield service outlook. During the second half of 2019, many oilfield service companies were surprised by the dramatic pullback in activity levels. Although we had been warning that operator budget exhaustion would occur in the first quarter of 2019, the majority of OFS companies were surprised by the dramatic pullback in activity levels. While commodity price volatility did not help, operators have remained focused on being disciplined with their spending. Also, increased frac efficiencies ended some completion programs earlier than expected.

Rising uncertainty in shale plays. We strongly believe that the NAM shale industry is maturing, and there will be greater differentiation in performance across the entire energy industry in 2020. Efficiency gains have plateaued across the U.S. Lower 48, and capital markets are not willing to fund growth, as in the past. This points to more uncertainty around expectations for U.S. oil production growth in 2020 than we have seen since the collapse of oil prices in 2014. Operators remain extremely disciplined with their spending levels, as the market demands they stay within cash flows. This has put additional pressure on OFS companies that are working hard to adapt to these shorter cycles in unconventional development. The key challenges for U.S. shale are: 1) consolidation has been slow to develop; 2) there are too many assets (DUCs) and companies in the field.

Technology revolution. We are convinced that technology will play a larger role in the oil patch in the near future. Historically, the industry has been a slow adopter of technology in favor of long-standing practices and legacy agreements with key contractors and suppliers. R&D spending across the sector has always been a small percentage of SG&A, approximately 0.5% of revenues. Today the push for greater efficiencies in the manufacturing mode of unconventional development is driving technological innovation.

Offshore upturn. We expect double-digit growth in offshore markets. We forecast that 2020 spending for the offshore sector will be up 10.3%, compared to 2019. We expect a squeeze on engineering capacity, on offshore assets, and on crews to become apparent as 2020 unfolds. Through innovation, cost reductions and reduced cycle times, the offshore industry is leaner and ready for a long, strong upcycle.

REGIONAL BREAKDOWN

North America. The pullback in U.S. land drilling started earlier in 2019 than in 2018, and the decline in the rig count was steeper than most companies had expected. Spending on U.S. land has generally been down in the low double digits, as the rig count continued to decline and operators remained disciplined with their capital spending. Some management teams described this volatility as the “new normal” for NAM unconventional development. We disagree. It is extremely challenging to build a sustainable business model, long-term, around this kind of volatility and with the lack of visibility that OFS companies currently have to their customers’ spending levels. A better approach is required. Our 2020 survey suggests capex will decline 6%, as operators remain disciplined with their capital spending. Consolidation among NAM operators will continue to have an impact on activity levels, as the combined entity typically spends less than the separate stand-alone companies.

Canada. For 2019, we estimate an 8.5% y-o-y decline in E&P capex, although 2020 is shaping up for 0.4% growth, which industry observers will likely take as a win. The Canadian Association of Oilwell Drilling Contractors (CAODC) forecasts 128 active rigs in the region for 2020, a roughly 4% decline below the 2019 YTD average. Meanwhile, the CAODC expects wells drilled in 2020 to be essentially flat, y-o-y. With $30 billion in foreign capital leaving the industry since 2017, along with nearly 30 high-spec drilling rigs, it’s easy to see why sentiment in Canada continues to be poor.

Middle East. In the Middle East, capital expenditures are set to rise 8% in 2020, y-o-y, although this follows a flattish 2019, which reflects reductions in output, due to OPEC agreements. We believe that the region will provide ample opportunity to grow the topline for service providers, although NOC customers have become more cost-conscious since the downturn. Conversely, geopolitical risk has increased this past year, as the spillover effects from a weakened Iran threaten to engulf nearby countries. Countering this are rumors of a potential deal to remediate relations between Qatar and the GCC contingent, which includes Saudi Arabia, the UAE, Bahrain and Egypt.

Russia/FSU. Capex in Russia and the FSU will grow 6%, y-o-y, in 2020, following a projected 8% decline in 2019. But downside risks are prevalent, due to OPEC compliance. We expect Lukoil, Gazprom and Rosneft to meet their production goals and investment plans, although recent production quotas could see spending underwhelm in 2020. The country is becoming an LNG supply behemoth, and pipeline gas exports are at record levels. Also, the recently commissioned Power of Siberia pipeline will connect to China and should alter energy politics going forward. EIA forecasts that gas production in Russia will increase 40%, over its projection period out to 2050, with Asia and Europe purchasing most of the new production.

Latin America. The market has been waiting several years for Latin American growth to break out. The quality of the resource was never a question, between the pre-salt fields offshore Brazil and the Vaca Muerta shale play in Argentina. The region experienced three years of spending declines in 2015–2017. Then there were two years of a rebound, with Latin American capex growing 19% in 2018 and 3% in 2019. Still capex remains well below 2013–2015 levels, as key countries are still experiencing increasing geopolitical instability and the impact from inflation. It will be challenging for Latin America to return to a sustainable period of capex growth without seeing more stability around Mexico, Brazil and Venezuela.

European spending is set to increase for a fourth straight year in 2020, for the first time since 2011–2014. From 2016, spending by select European companies has grown 26% and has moved above 2015 spending levels. However, looking back at our 2019 capex survey, we initially estimated that spending would grow 1%. We increased our estimate to 3% at our mid-year survey and again have revised 2019 higher to 11%. The upside has been driven by spending by new regional operators, as private equity-backed independents have acquired assets from the majors. However, we are starting our survey process expecting 1% growth in 2020.

Asia/Australia capex for 2020 is projected to gain just 1% after a 13% increase in 2019. Despite the large drop-off, we see a number of positive trends in the region that should be a boon for offshore drilling and service providers. With a number of project starts by Woodside, CNOOC, Medco Energi, Premier Oil and Shell, the region is set to prosper, even while several majors/IOCs exit the region.

Africa. We project that spending in Africa will increase 3% in 2020, following a 9% jump in 2019. A more malleable stance from local governments, combined with offshore drilling campaigns being implemented by IOCs and independents, points to solid activity. However, we don’t rule out political risk. Algeria is a prime example of stability, while unfavorable regulations toward E&Ps in Nigeria point to unrest. Overlay increased investments from LNG projects in Mozambique, Nigeria LNG Train 7, and Rovuma, and our base case estimate of 3%, y-o-y, growth in regional spending seems sturdy.

- The last barrel (February 2024)

- E&P outside the U.S. maintains a disciplined pace (February 2024)

- Management issues- Dallas Fed: Activity sees modest growth; outlook improves, but cost increases continue (October 2023)

- Executive viewpoint (April 2023)

- Global offshore market is on the upswing (April 2023)

- The last barrel (March 2023)

- Applying ultra-deep LWD resistivity technology successfully in a SAGD operation (May 2019)

- Adoption of wireless intelligent completions advances (May 2019)

- Majors double down as takeaway crunch eases (April 2019)

- What’s new in well logging and formation evaluation (April 2019)

- Qualification of a 20,000-psi subsea BOP: A collaborative approach (February 2019)

- ConocoPhillips’ Greg Leveille sees rapid trajectory of technical advancement continuing (February 2019)