United States: U.S. drilling

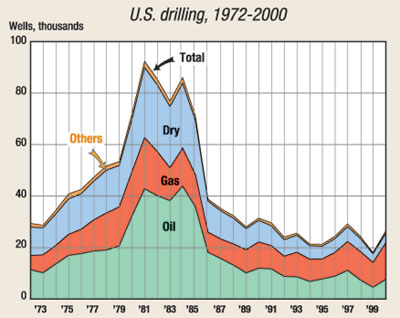

U.S. DRILLINGRecovery should come in second halfThe banner year for drilling originally expected for 2001 was first interrupted by a full-blown recession in the U.S., only to be blindsided by the terrorist atrocities of September 11. This combination caused a dramatic drop in oil consumption, which prompted oil price declines of 35% to 38% (depending on the benchmark) between the beginning and end of 2001. Not surprisingly, drilling activity quickly followed suit, as the U.S. active rig count plummeted more than 19% by year-end. However, despite getting off to a slow start, there are positive indications that 2002 will see the decline reversed, and drilling activity return to healthier levels. The leading cause for optimism is OPEC’s decision to cut its oil production quotas by 1.5 million bpd this month. Taken with last year’s reductions, the January cuts will put OPEC’s 2002 quotas about 5 million bpd below those of 2001. The net effect, barring any further economic calamities, should be rising E&P activity during the second half this year. Highlights of World Oil’s forecast for 2002 include:

Oil and gas prices. Although the terrorist attacks were a graphic example of how extraneous factors can affect overall supply / demand balances, one fact remains – the U.S. and the rest of the world’s oil markets still depend on the whims of an OPEC driven by Saudi Arabia, Kuwait and the United Arab Emirates. Fortunately, their current whim is to strengthen prices rather than market share, which facilitated their agreement with non-OPEC producers to cut production. OPEC’s 5-million-bpd quota reduction, if honored by all, will actually cut oil production by around 3 million bpd, compared to 2001 levels, which would be more than enough to offset the demand losses that occurred since 9/11. Then, assuming these conditions come to pass, average WTI price in 2002 will approach $28 per bbl. Natural gas is another story. The recession-induced reductions in industrial gas consumption, plus a thus-far, milder-than-normal winter, have led to unusually high storage levels. However, the dramatic drop in drilling, combined with steep reservoir depletion rates (many new offshore fields have exhibited decline rates of 50% per year, for example) could wipe out the current surplus by spring. This, and an improving U.S. economy, are expected to send average U.S. wellhead gas prices to above $4.00 per Mcf this year. Operator surveys. World Oil’s year-end survey of 17 U.S. major drillers (integrated companies and independents with large drilling programs) and 140 independents indicates only moderately weakened expectations for 2001. Majors plan 5,488 wells, down 8% from last year. Independents responding will drill 1,252 wells, a decline of only 3%. The majors are pulling back in terms of exploration this year, with nearly 8% of their wells targeting wildcat prospects, compared to 9% in 2001. Exploration by independents will rise to about 28% of total drilling, compared to 26% a year ago. Salomon Smith Barney’s annual year-end survey of 243 U.S. and international operators indicates that worldwide E&P budgets will decline 0.5% this year. This follows a 25% growth in 2001, the highest year-to-year increase since 1981. Respondents’ spending plans are based on an average oil price assumption of $20.72 per bbl. For the U.S., the Salomon survey indicates total E&P spending of $28.7 billion this year, a decrease of 12%. The majors see their spending falling 2% this year, but the independents are more pessimistic and project expenditures to drop by 19%. The apparent conflict between the World Oil and Salomon surveys is likely due to the fact that the World Oil sample includes more small independents with less expensive, lower risk operations. Area forecasts. The following summaries represent important states or regions that greatly influenced the 2002 forecast. Activity in the Gulf of Mexico will likely be the most severely affected by the turndown in oil and gas prices, with drilling predicted to decline nearly 21% to 767 wells. But a look at rig activity by mobile rig type indicates that high-risk, expensive deepwater drilling is faring better than shallower water, on-the-shelf operations. As 2002 began, there were 200 mobile rigs available in the Gulf, 84 of which were not working. Of these idle rigs, 71 were jackups and four were submersibles. Of the semis in the Gulf, 29 out of 38 were employed, and all eight drillships were working. Texas, the country’s largest drilling state, is also faring better than most of the rest of the U.S. Adequate infrastructure, nearby markets and tightly controlled operating costs still in place as a result of the 1999 downturn all contribute to operators’ being able to profit even with oil just below $20. Oil and shallow gas drilling will keep the state’s well count (7,384 wells) within 6% of last year’s figures. The state’s bright spot will be in District 9 where the Barnett Shale development predominates. Some 913 wells are forecast, for an 18.7% increase, as rigs continue to be added in the district. The three Texas Railroad Commission districts that encompass the oil-prone West Texas region are all indicated to decline less than the national norm. District 8, which once was the largest in terms of wells drilled, will drop to number three, as activity falls 5.8% to 870 wells. A little further north, District 8A should record the smallest percentage decrease within the state, at 2.6%. District 7C will not perform as well, as 854 wells are expected, for a drop of 7%. District 4 in extreme South Texas should hang on to its title of number one in drilling, even though natural gas is still the preferred target. A minimal 3% reduction in activity there should produce 1,100 wells this year. Being reliant on gas development, particularly in the southern half, Louisiana will see drilling drop off by 7% to 1,460 wells. However, the state is in position to quickly benefit from improved gas prices when they come to pass. Oil prices, which are less erratic than gas prices, should help the northern half of the state perform a little better than the southern half. As a result, North Louisiana drilling should total 882 wells. California’s mostly shallow-depth, heavy oil fields are highly susceptible to oil price fluctuations, and thus took a beating during 1999. Then, in late 2000 and early 2001, extremely high gas prices caused even more problems, as the cost of this fuel, which is used to generate steam, clobbered the economics of most steam-injection oil recovery projects. Additionally, the state’s electricity shortages earlier this year had the regulators threatening to take control of private steam generation facilities for use in power generation. Unfortunately, the low-margin economics of California’s heavy oil projects will continue to be impeded by current oil prices. Consequently, a 9.8% decline in drilling is expected. However, as demonstrated by the dramatic turnaround during 2000, these projects allow the state’s operators to react very quickly, thus, if prices do improve, this forecast will be exceeded easily. Coalbed methane development programs will again be a major portion of Rocky Mountain drilling this year. And since coalbed methane has been demonstrated to be profitable, even with low gas prices, the region’s activity will not decline as abruptly as the rest of the country. Collectively, Rocky Mountain wells should fall from 7,589 in 2001 to 7,216 in 2002. Wyoming is home to most of it, and will see drilling drop a mere 2% to 4,900 wells in 2002. If coalbed wells are excluded, Wyoming should see 600 conventional wells this year compared to 700 wells in 2001. A lower percentage of Colorado’s wells target coalbeds, so their number will not be able to mask the expected decline in conventional drilling. Consequently, an 11% decrease to 1,246 wells is anticipated this year. In the Mid-Continent area, Oklahoma will experience a 20% reduction in activity to 2,047 wells. Gas development is being impacted by current prices, especially among the majors, and its mature oil fields require stable oil prices. Kansas is predicted to have a so-so year too, as drilling falls 13% to 1,395 wells. The state is heavily gas-oriented with its giant Hugoton field and operators are awaiting higher gas prices.

|

- Prices and governmental policies combine to stymie Canadian upstream growth (February 2024)

- U.S. producing gas wells increase despite low prices (February 2024)

- U.S. drilling: More of the same expected (February 2024)

- U.S. oil and natural gas production hits record highs (February 2024)

- U.S. upstream muddles along, with an eye toward 2024 (September 2023)

- Canada's upstream soldiers on despite governmental interference (September 2023)

- Applying ultra-deep LWD resistivity technology successfully in a SAGD operation (May 2019)

- Adoption of wireless intelligent completions advances (May 2019)

- Majors double down as takeaway crunch eases (April 2019)

- What’s new in well logging and formation evaluation (April 2019)

- Qualification of a 20,000-psi subsea BOP: A collaborative approach (February 2019)

- ConocoPhillips’ Greg Leveille sees rapid trajectory of technical advancement continuing (February 2019)